Yahoo Finanzas

Yahoo Finanzas Why W. P. Carey Is a Great Inflation Hedge

In my opinion, W. P. Carey Inc. (NYSE:WPC) is one of the best REITs for hedging portfolios against inflation and possible recession. Only a few similar stocks enjoy the ~8% year-over-year historical gains of W. P. Carey, which has seen even faster growth of 27.5% over the past five years. The stock also has a Quant Rating of strong buy and scores a 7 out of 10 for profitability on GuruFocus.

Inflation on the rise

It's not a matter of when but how deep will the torrents of inflation and recession will cut into economic growth. Stagnation is the immediate fear. Depression looms in the shadows. However, one of the best was that investors can hedge their nest eggs is by investing in REITs, as the value of real estate tends to hold up incredibly well in the long-term.

Inflation is primarily attributable to the Federal Reserve's record easy-money policies and money-printing during the Covid-fueled economic downturn. These policies were equal to borrowing money from the future. Now, due to Russia's invasion of Ukraine contributing to inflation spiraling completely out of control, the Fed needs to front-load rate hikes.

Then there are undertows from growing consumer trepidations. A Jefferies survey reports there is "weaker financial confidence, perceived purchasing power, and (higher) future inflation expectations" among consumers regardless of income... Overall, 54% of consumers surveyed said they are less confident about their finances vs. 17% more."

Why W. P. Carey?

W. P. Carey is a diversified net lease real estate investment trust (REIT) that specializes in the single-tenant properties markets in North America and Europe. W. P. Carey offers property sales and leasebacks, build-to-suit custom-designed new facilities and financing upfront expenses. The company is currently celebrating its 50th anniversary.

William Polk Carey, for whom the company is named, began his career pooling net-leased commercial real estate assets for individual investors. He built the market cap to an astounding $16.05 billion.

In approximate numbers, the company boasts more than 1,304 net lease properties. They occupy 156 million square feet. The occupancy rate is a sky-high 98.5%. Sixty-three percent of their properties are in the U.S. and 35% are in Europe. The rest are in Canada, Mexico and Japan. For the property type breakdown, 17% is retail space, 19% is office space, 23% is warehouse, 26% is industrial and the rest is storage and other.

For years, I have been bullish on W. P. Carey. It just keeps on making money for investors like the Energizer (NYSE:ENR) bunny.

Recently, first-quarter earnings topped the consensus estimates. First-quarter adjusted funds from operation (FFO) per share of $1.35 beat the average estimate of $1.24. The results increased from $1.22 in the year-ago quarter. Real estate adjusted FFO of $252 million increased from $239.0 million, or $1.27 per share, in the fourth quarter of 2021 and from $210.3 million, or $1.19 per share, in the first quarter of 2021. Earnings are nearly 10% over quarterly FFO per share.

W. P. Carey also raised its full-year adjusted FFO per share guidance to a range of $5.18 to $5.30 (consensus calls for $4.97), including real estate adjusted FFO per share of $5.03 to $5.15.

Reflecting on inflation and rate hikes, CEO Jason Fox observes that "over 99% of our ABR comes from leases with embedded rent growth, the majority of which is tied to CPI. We continue to feel good about the all-in returns we are earning for our investors relative to our cost of capital. In fact, for investments with rent increases tied to CPI, higher expected rent growth in the near term may partly compensate for a higher cost of debt."

Much of the average base rent at W. P. Carey is from industrial real estate and warehouses. Industrial companies prefer leasing rather than owning their premises. Trade troubles with China and sanctions on Russia are giving impetus to the industrial real estate boom in the U.S. The trend is likely to continue for the foreseeable future.

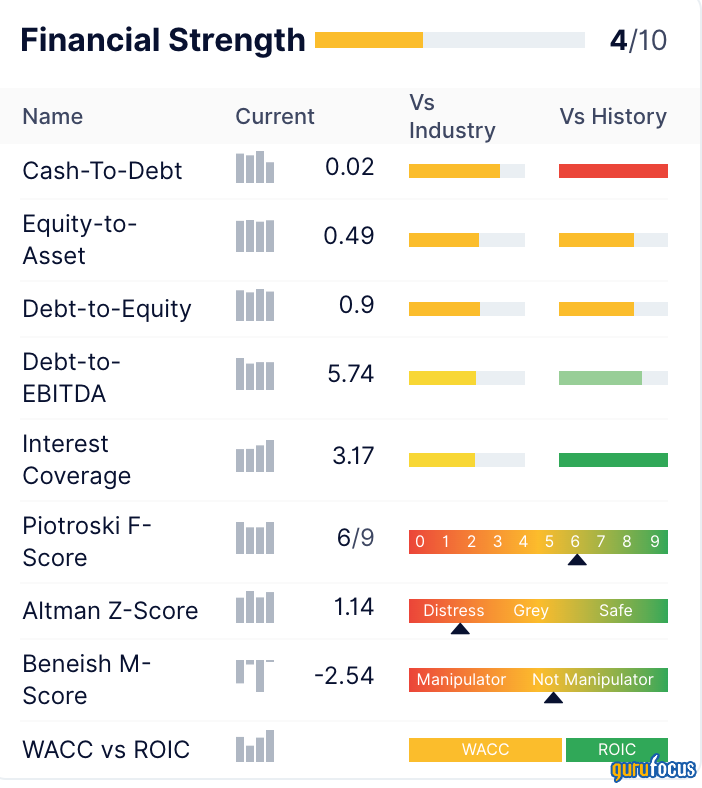

Financial strength

A risk to consider is the company's low financial strength. GuruFocus ranks the financial strength at 4 out of 10.

Despite inflation and interest rate hikes, Fox told investors in last week's report that W. P. Carey locked "in an attractive cost of debt on it significantly lower than current market interest rates. Second, our cost of equity has improved meaningfully since late February with our stock currently trading around its highest level since late 2019, before the onset of COVID."

The company's balance sheet and market cap offer near limitless opportunities for access to attractively priced long-term capital. I am confident that the company can continue taking on more debt as needed due to access favorable rates, even if other companies would be crushed under so much debt.

The company also seems confident that its debt is under control considering the high dividend. The company has a 12-month forward dividend of $4.23; that is a yield of 5.2% at the current price. If inflation persists and a recession begins, REITs are a good hedge and provide diversification for portfolios.

Value

One advantage W. P. Carey shares have is that they are not particularly volatile. The beta of W. P. Carey is 0.38, which is far lower than the market volatility rating of 1. Over the past year, the share price has increased 17%. The price is up over 36% over the past five years. The only significant tumble coincided with the mid-March 2020 market crash.

The company is further reporting its collection rate was steady, hitting 99.7% for the quarter. Portfolio occupancy was 98.5%, unchanged from the previous quarter. Investment volume of $415.4 million was completed year-to-date. Gross disposition proceeds were $26.6 million during the quarter.

Analysts on Wall Street overwhelmingly give W. P. Carey buy and strong buy recommendations. There are a few hold recommendations and no one on Wall Street is suggesting investors sell their shares as of this writing. Short interest is a measly 1.85%. News sentiment is overwhelmingly positive. Technicals are positive. The return on equity is 5.67% and asset growth is 5.26%.

The trend among corporate insiders is heavily on the buy-side as well. The company has a healthy and diverse mix of shareowners:

In my opinion, any price below the $80 mark would look undervalued for this stock. At Friday's closing price of $77.90 per share, the GF Value chart rates the stock as fairly valued.

This article first appeared on GuruFocus.